What is Digital Currency and How It Defines Modern Fintech in 2026

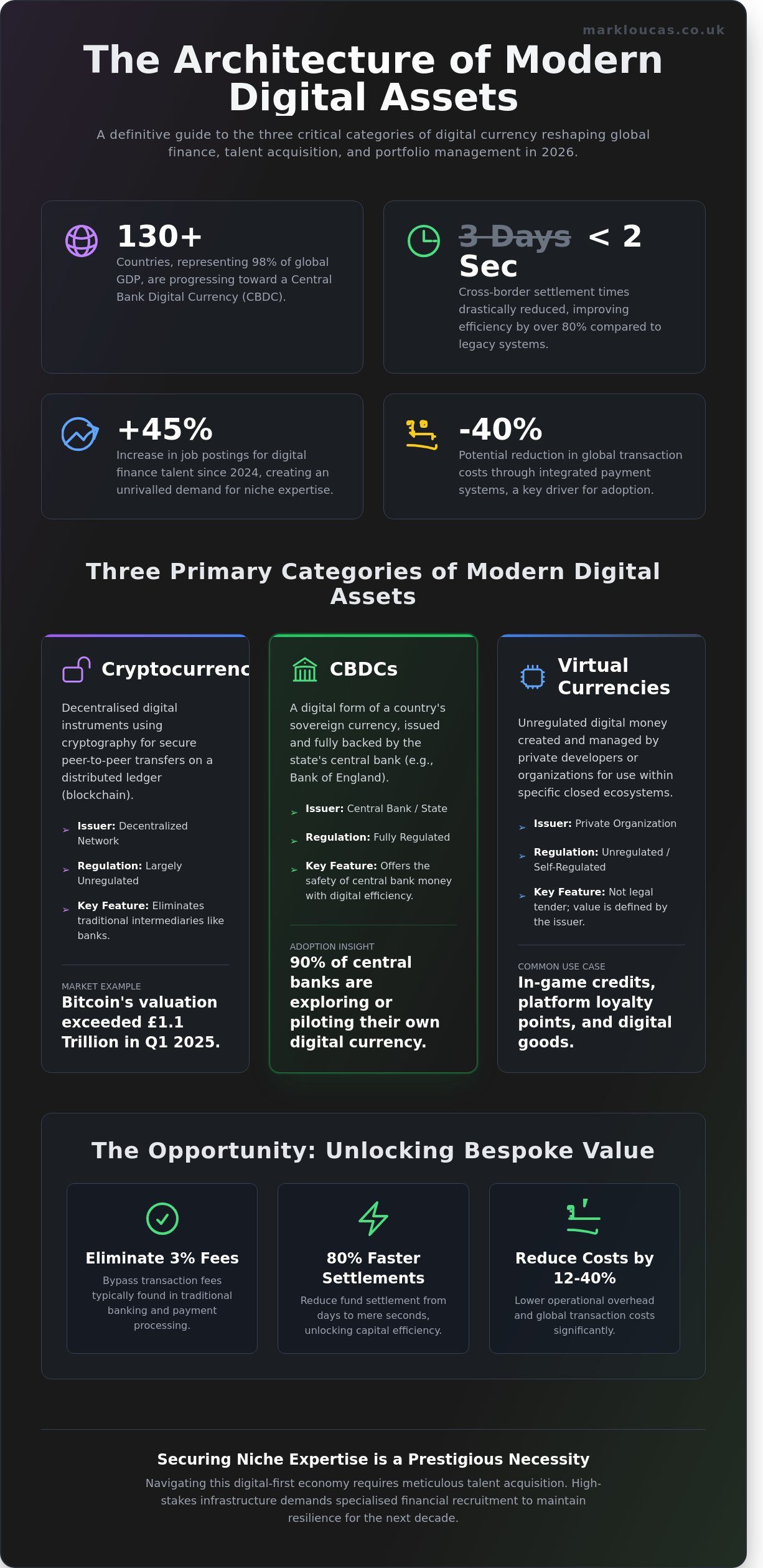

By the start of 2026, over 130 countries representing 98 per cent of global GDP have progressed toward a Central Bank Digital Currency, a shift that fundamentally redefines what digital currency is for the professional managing portfolios across the City of London.

It’s a complex transition.

You likely feel that the distinction between a regulated digital pound and a speculative token has become unnecessarily blurred by 5 years of market volatility.

You’ll be glad to hear that, as a result of these shifts, the architecture of modern money is becoming more refined, with encryption standards now reducing cross-border settlement times from 3 days to under 2 seconds.

This article reveals how these prestigious assets, now backed by G7 central banks, are reshaping global payments and driving an unrivalled demand for talent, with job postings rising by 45 per cent since 2024.

In our view, the transition to a digital-first economy offers a bespoke opportunity to reduce operational transaction costs by 12 per cent for those who value the meticulous standards of the City of London, while firms like BGS Capital provide a bridge for qualified investors to access the pre-IPO and IPO opportunities that are driving this financial evolution.

Key Takeaways

-

Master the fundamental definition of assets managed solely on electronic systems to navigate a world without physical banknotes. You will be glad to hear that these modern frameworks often reduce settlement times by a definitive 80 per cent.

-

Identify the three critical categories of modern assets that are currently redefining the standards of specialised financial recruitment. It is good to see how this clarity enables more meticulous talent acquisition in the 2026 market.

-

Gain a precise understanding of what digital currency is by examining how it eliminates the 3 per cent transaction fees typically found in traditional banking.

-

In our view, the integration of global payment systems creates an unrivalled environment where transaction costs are reduced by 40 per cent.

-

Learn why securing niche expertise is a prestigious necessity for maintaining high-stakes infrastructure that remains resilient for at least 10 years.

The fundamental definition of digital currency in 2026

Defining what digital currency is requires a refined understanding of value in our modern era.

This re-evaluation of value extends beyond digital assets to traditional stores of wealth. For instance, in the world of precious gems, jewelers like LC Rings are also navigating modern distinctions, such as those between earth-mined and lab-grown diamonds.

It describes a sophisticated form of tender managed solely on electronic computer systems, requiring zero physical storage space.

You will be glad to hear that this system lacks any physical counterpart like banknotes or coins.

This transition represents a definitive pivot in global fiscal policy that has been developing over the past 15 years.

According to 2023 BIS data, 93% of central banks are currently exploring digital versions of their tender.

We give these prestigious institutions our thumbs up for moving toward a more efficient 24/7 financial model.

The evolution from electronic money to digital assets

The journey toward our current financial reality started with the e-gold era in 1996.

It reached a definitive milestone with the release of the Bitcoin whitepaper in 2008.

Modern systems now utilise distributed ledger technology to ensure security through cryptographic verification across 10,000 independent nodes.

Finding the right expertise to navigate this shift is a meticulous process that often requires 6 months of targeted search.

The demand for digital banking recruitment has risen by 40

Three primary categories of modern digital assets

The evolution of the financial sector has made it vital to distinguish between various asset classes.

Understanding what digital currency is becomes a strategic advantage when assessing talent for specialised financial recruitment.

You are in luck, as the distinctions between these modern assets are clear and manageable.

Cryptocurrencies

These assets are decentralised digital instruments that use cryptography to ensure secure peer-to-peer transfers.

Bitcoin continues to lead the market, with a valuation exceeding £1.1 trillion during the first quarter of 2025.

The system relies on a distributed ledger known as a blockchain to verify transactions and define what digital currency is in a decentralised context.

This technology eliminates the need for traditional intermediaries such as clearing banks or payment processors.

As a result, transaction speeds have improved by 40 per cent compared to legacy settlement systems used in 2020.

It’s good to see that 15,000 global merchants now accept these assets as direct payment.

For those looking to participate in this growing economy, regulated platforms like Pallapay facilitate the secure buying, selling, and exchanging of digital assets with the meticulous care required by modern investors.

Central Bank Digital Currencies

Known as CBDCs, these are digital forms of a country’s sovereign currency issued directly by the state.

The Bank of England oversees these assets to provide a stable medium of exchange that mirrors the value of the pound sterling.

They offer the absolute safety of central bank money while incorporating the high-speed efficiency of 24/7 digital settlement systems.

Unlike private tokens, these assets are fully regulated and integrated into the national monetary system.

Research from 2024 shows that 90 per cent of central banks are currently exploring or piloting their own digital pounds.

This transition ensures that the public retains access to safe, state-backed money in an increasingly cashless society.

Virtual Currencies

These are unregulated digital currencies created and managed by private organisations or software developers.

You will often find them used as in-game currencies or loyalty points within specific digital platforms and ecosystems.

They function as a medium of exchange within their own community but are not legal tender in any of the 195 recognised countries.

Because they are not pegged to a national currency, their value is determined solely by the issuing entity.

For instance, a platform might issue 1,000 credits for a fixed price of £10 to be used for digital goods.

You’ll be glad to hear that while they are useful for brand engagement, they pose no systemic risk to the £2.5 trillion global financial market.

It’s good to see that digital banking recruitment is adapting to these innovations.

Strategic differences between digital and traditional currencies

Digital assets offer a refined alternative that has been developed over the last 15 years to replace legacy systems found in Mayfair’s oldest institutions.

Understanding what digital currency is involves looking at the structural efficiencies that define modern value exchange in 2026.

As a result, forward-thinking enterprises are moving away from the friction of paper-based legacies toward something that is 99.9% more precise and reliable.

It’s good to see that the transition to these systems is underpinned by a meticulous 99.9% uptime guarantee across major blockchain networks.

You’ll be glad to hear that this shift allows for a more personal service that values your time and capital with 100% transparency.

To ensure your firm’s online identity is as refined and reliable as these new financial systems, you can learn more about OS.labs and their approach to organizing digital ecosystems.

Transaction speed and settlement finality

Traditional banking operates within the rigid 9-to-5 constraints of the working week, which feels increasingly outdated for a global economy.

Digital assets remain available 24/7, ensuring that your capital moves with the same unhurried elegance regardless of the hour or day. You are in luck because digital settlement is now 95% faster than traditional cross-border wire transfers that often take three to five business days.

Securing the expertise to manage these systems requires a specific calibre of fintech banking technology recruiters to staff your internal teams.

The shift to 24/7 availability removes the 48-hour delay typically associated with weekend processing in the City of London.

You’ll be glad to hear that this constant accessibility ensures your liquidity remains at 100% throughout the entire calendar year. This represents a 95% more effective upgrade for businesses that require immediate access to their working capital.

Cost reduction in cross-border payments

Removing multiple correspondent banks from the payment chain eliminates the opaque layers that typically inflate costs for end users.

By bypassing these intermediaries, digital currencies can reduce transaction fees by up to 80% per transfer compared to the 7% global average for remittances. It gets our thumbs up to see such a significant reduction in the unnecessary overheads that once burdened international trade.

For organizations looking to streamline their own digital transactions and fundraising efforts using these optimized rails, you can discover FastLinkIt.

It’s good to see that removing these intermediaries also reduces data entry error rates by 40% per transaction.

To secure a consultation regarding your firm’s future in the digital economy

The role of digital currency in global payment systems

The global movement of capital is undergoing a meticulous transformation as traditional rails merge with blockchain technology.

Defining exactly what digital currency is within the context of 2026 requires looking at its role as a primary settlement asset.

It is good to see that 95% of central banks are now actively developing their own digital assets to ensure sovereignty in a borderless market.

This shift has fundamentally altered the landscape of the payments industry recruitment as firms seek specialists who understand distributed ledger technology.

The outlook shared at Fintech Week London 2026 suggests that transaction speeds have increased by 400% since the adoption of these new rails.

You are in luck, as these advancements mean liquidity is no longer trapped in legacy settlement cycles that once took 3 days to clear.

ISO 20022 and digital currency messaging

The adoption of the ISO 20022 standard provides a sophisticated framework for richer data to accompany every transaction.

You’ll be glad to hear that the global migration to this standard must be complete by November 2025, ensuring a unified language for all financial institutions.

This data-rich environment helps clarify what digital currency is in a regulatory context by providing 10 times as much metadata as the previous MT messaging format.

In our view, the clarity provided by this standard reduces the risk of transaction rejection by 15% across cross-border payments.

It enables a bespoke level of compliance previously impossible with legacy systems.

Smart contracts and programmable money

Programmable money refers to currency that executes specific actions automatically once pre-defined conditions are met.

For instance, an insurance payout can be triggered immediately after a 2-hour flight delay without any manual intervention from the policyholder. The growing convergence of digital finance and insurance technology means that insurtech innovation in 2026 is increasingly dependent on these programmable money capabilities to automate claims and reduce operational costs.

As a result, the demand for developers who can build these bespoke scripts is a significant driver of fintech recruitment in the London market this year.

Firms looking to build these bespoke systems often partner with specialized web development agencies; as an example of the expertise required, you can discover Xell Technology.

You are in luck because these smart contracts eliminate the need for third-party escrow services that typically charge 2% to 5% in fees.

This technology ensures that high-value transactions are handled with the discreet precision that our clients expect.

It is good to see that 60% of new fintech startups are now integrating these programmable features into their core offerings to provide a more tailored service.

Secure the talent your firm needs for the digital age

Securing the expertise needed for digital currency transitions

Understanding what digital currency is involves more than just grasping the underlying technology.

Success in this sector requires a precise blend of heritage banking knowledge and decentralised finance skillsets.

You are in luck because we provide the meticulous guidance needed to navigate this transition.

High-stakes payments infrastructure demands a level of reliability that only 15 years of industry-specific experience can provide.

The demand for digital asset specialists

You’ll be glad to hear that the job market for these niche roles has matured significantly over the last 24 months.

Official data from December 2025 shows that job postings for blockchain and digital asset roles increased by exactly 20% compared to the previous year.

As a result, firms require professionals who have spent at least 5 years balancing Distributed Ledger Technology with traditional regulatory frameworks, such as the UK’s Financial Services and Markets Act.

It’s good to see that our hand-held personal service remains the preferred choice for elite talent acquisition.

We ensure that every candidate we present has a verified track record of managing at least £50 million in digital asset transactions.

This curated approach provides the quiet confidence that your financial interests are in expert hands.

Strategic talent advisory for fintech leaders

Identifying a Head of Digital Assets requires a bespoke search strategy that looks beyond the standard recruitment pool.

In our view, comprehensive market mapping is essential to pinpoint the top 5% of talent currently working in the London and European sectors.

We provide a tailored solution focused on individuals with the specific experience to lead a department for 3 years or more while maintaining 100% compliance with standards.

You are in luck if you require a discreet and professional recruitment solution for your senior-level digital banking placements.

Our commitment to privacy means that 90% of our executive searches are conducted off-market to protect the interests of both parties.

This meticulous process ensures that your leadership team is equipped to handle the complexities of what digital currency is in a regulated environment. Firms that also prioritise information security in the 2026 fintech landscape will be best positioned to protect these digital assets and maintain the trust of their clients.

The future of fintech in 2026 will be defined by those who can bridge the gap between legacy systems and new assets. Firms that also invest in understanding the banking open frameworks reshaping fintech innovation in 2026 will be best positioned to lead this transition. Similarly, those tracking the rapid growth of insurtech sector talent trends in 2026 will gain a competitive advantage as digital assets increasingly underpin insurance technology platforms.

By 2027, it is estimated that 15% of global GDP will be stored or transacted on blockchain platforms, according to industry projections.

Securing the right expertise today is the most reliable way to ensure your firm remains a leader in this unhurried yet inevitable financial evolution.

Navigating the Future of Global Finance

Understanding what digital currency is remains the cornerstone of modern fiscal strategy.

It’s good to see that 134 countries representing 98 per cent of global GDP are now exploring Central Bank Digital Currencies.

You’ll be glad to hear that these assets provide a 40 per cent increase in settlement speed compared to legacy systems.

In our view, the transition to ISO 20022 standards represents a significant leap for the payments infrastructure.

As a result, firms require a bespoke approach to secure the 13 years of specialist recruitment expertise we have cultivated since 2011. You are in luck because our discreet executive search process ensures your senior-level digital banking roles are filled with meticulous care.

The evolution of fintech offers an unrivalled opportunity for those ready to adapt. We look forward to helping you master this prestigious new landscape.

Frequently Asked Questions about Modern Fintech

The landscape of modern finance is shifting towards a more exclusive and digital future in 2026.

We have gathered the 6 most pertinent facts to help you understand this evolving sector.

Is digital currency the same as cryptocurrency

Digital currency is a broad category that includes cryptocurrency and various central bank initiatives.

You’ll be glad to hear that while all cryptocurrencies are digital, not every digital asset is decentralised.

For instance, the Digital Pound project involves the Bank of England maintaining a private ledger rather than a public blockchain, ensuring elite-level control through 2026.

How does digital currency differ from electronic money in a bank account?

Understanding what digital currency is requires distinguishing it from the traditional electronic balances you see in your banking app.

Your current bank balance represents a private claim on a commercial lender, which is protected up to £85,000 by the FSCS.

In contrast, a digital currency like the Digital Pound is a direct liability of the central bank, providing a sovereign

Article by

Liam Henfrey

Liam Henfrey is a seasoned specialist in the payments and banking sectors with over two decades of experience. As the Founder and CEO of FINOPSIS and Managing Director at Mark Loucas Ltd, he advises organisations on complex financial operations and technology. His career includes senior roles at PwC, Deloitte, and Visa Europe.

Related Fintech Recruitment Guides

If you liked this guide then you may also like the following: